![]()

The Month That Was-September 2017

MARKET SUMMARY: Plodding Higher

After spending considerable time contemplating the best way to describe the current market after a Summer of low volatility and steady upward movement, we’ve settled on a rather benign word: Plodding.

Oxford Dictionary defines Plodding as slow-moving and unexciting. The irony of such a peaceful market co-existing in a world of geo-political concerns with potentially destructive conflict (think N. Korea), as well as continuous societal anxiety and unrest (Trump vs. Everyone) isn’t lost on us.

SO how can we explain this calmness in the face of such clear and obvious threats to peace and tranquility? How can markets follow this path while there exists such divisiveness and feelings of unease among so many? How can the market shrug off all the seemingly awful news we see on our TVs and in social media on a daily basis?

Perhaps the best explanation is indeed the simplest: It’s the economy!!!

While domestic growth has been steady, albeit unspectacular, economies across the globe have strengthened over the course of the year, led by gains in Europe, Asia and Emerging Markets. Strong global economic growth has filtered through to individual U.S. companies, which have generally exhibited positive momentum in their earnings reports. And this, in turn, continues to support our slowly expanding (dare we say plodding) US economy as a whole.

Over the course of September, the economic data continued along the line we have been accustomed to over the past few years: unspectacular but solidly expansionary. This baseline scenario continues to support the modest level of approximately 2% GDP growth. And as we have seen, this level of growth appears to be sufficient to support market gains. Probably most importantly in this regard, the data points continue be void of any meaningful signs of impending recessionary pressures.

As we enter the 4th quarter of 2017, we will continue to monitor markets, corporate earnings, and both domestic and global economies for signals of continued (and hopefully expanded) growth. While we continue to maintain our recent analytic framework of viewing the markets through a fundamentals + DC lens, we are comforted by markets’ apparent prioritization of fundamental economic data.

CLOSED-END FUND (CEF) COMMENTARY: CEFs Fully Recover From the Summer’s “General Widening”

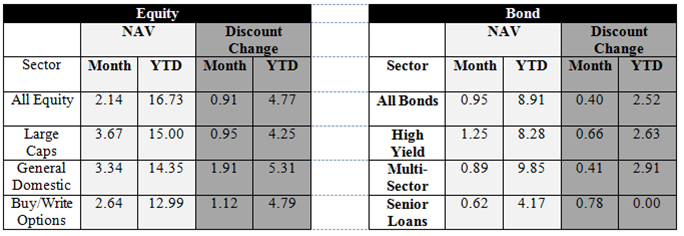

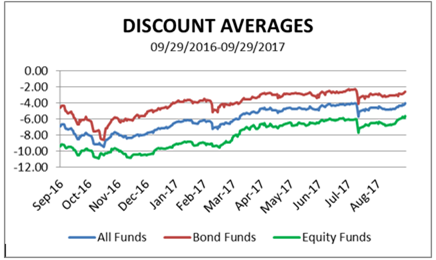

September was a strong month for CEFs both in terms of NAV growth and discount movement. On the NAV side of things, and as shown in the table below, both equity and bond funds posted solid gains. In regards to discounts, and as shown in the one year chart above, CEFs continued the general path of narrowing we have experienced throughout 2017. However, upon closer look, we can also see that in September, CEFs fully recovered from the “general widening” that occurred in the latter part of the summer, which will be the subject of this month’s commentary.

In late summer, CEFs experienced a “general widening” period in which discounts across the board widened-out causing reductions in the prices of CEFs overall. As we have discussed in the past, these “general widening” periods are typically caused by 2 factors which lead to excessive selling pressures (which usually occur at the same time): 1) fear based selling and 2) forced liquidations. These periods can be broken down into 3 stages:

1) Excessive Selling Pressures cause CEFs to trade lower than any inherent losses and discounts widen across the board.

2) A Stabilization of Discounts occurs once the excessive selling pressures cease.

3) Discounts Rebound as buyers return and purchase CEFs at attractive levels.

Here is a simplified description of such periods: Excessive selling leads to large declines in the overall markets. When sellers outnumber buyers, prices fall. These declines can also lead to investors being forced to sell, for reasons such as margin calls. Through the excessive selling, CEFs widen.

So how does this get resolved? The first step is the cessation of the fear based forced liquidation pressures. This can occur for a variety of reasons, including a resolution to any concern that has caused the selling pressures in the first place. Once the selling subsides in the overall markets, this will also typically lead to a cessation in the selling pressures caused by any forced liquidations. (As we have mentioned in the past, 10:00 and 2:00 are the traditional times by which margin calls have to be resolved, so we are always watching movements around those times). Once the selling pressures end, and buyers and sellers regain a more equilibrium level, CEFs stabilize.

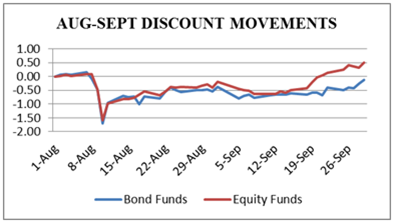

At this point, it is typical that opportunistic investors (like us) come in to swoop up the bargains and discounts narrow back. However, depending upon the circumstances, the stabilization period can last a period of time prior to the full bounce back from opportunistic buyers. The graph below shows how discounts moved during the recent widening.

While widenings occur from time to time (usually once or twice a year), the root catalyst and duration of the stages will vary. In this summer widening, we can see that the excessive selling pressures, although dramatic, last solely two days. And while, there was a rather nice bounce back on day 3, the next few weeks were probably better placed in the stabilization stage. Then, starting in Mid-September, we truly entered the final stage of the cycle as discounts fully recovered.

While the over cycle of a “general widening” returns CEFs back to their original levels, the understanding of the cycle is an important tool for our portfolio management. Through the recognition that these widenings are temporal in nature, we are able to take the appropriate actions in identifying and effectuating opportunities in our CEF investments.